Banks issue secured and unsecured loans to customers for specific needs, the foremost criterion being the ability to repay the loan on time. To monitor individuals’ credit behaviour, credit agencies compile data on all loans, credit cards, and other lines of credit. The most authentic of these is CIBIL in India, the Credit Information Bureau of India Ltd. Lenders look for customers with a sound credit history and a good CIBIL score. This write-up will help our esteemed customers understand ‘what is a CIBIL score’ and the details of the CIBIL Score.

What is a CIBIL Score and Why is it Important?

The CIBIL Score has become a priority for Banks and NBFCs; further credit is granted based on the applicant’s credit report, and an individual rating is assigned to an individual based on the performance of the various credit lines used by TransUnion CIBIL, reflecting creditworthiness.

Every time a Bank receives a loan or credit card request, an enquiry is forwarded to CIBIL to obtain the individual’s CIBIL score and history. A higher credit score means that you are a more reliable borrower, and lenders have to bear a lower risk while lending you money. Applicants with a CIBIL score of 750 or higher are offered higher loan amounts with better terms and conditions.

What is a CIBIL Score Range and What Does It Mean?

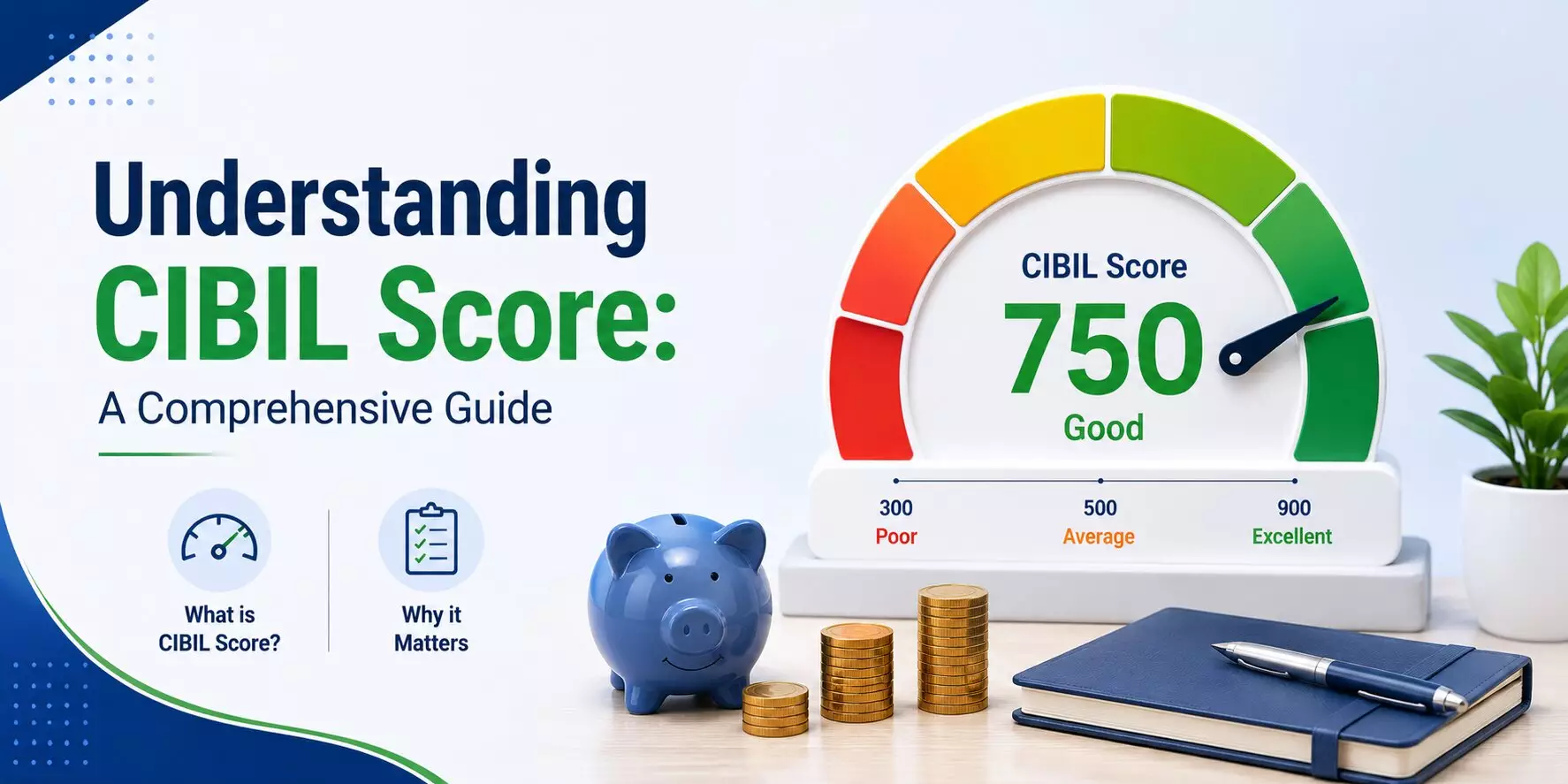

The CIBIL Score range is 300 to 900; scores closer to 900 indicate a low risk, while scores closer to 300 indicate a high risk.

| CIBIL SCORE RANGE |

SIGNIFICANCE |

CREDIT QUALITY |

|

Below 300

|

Below six months of credit usage

|

Very Poor

|

|

300 – 550

|

Low score not eligible for credit

|

Poor

|

|

550 – 620

|

Credit issues. Poor credit history

|

Fair

|

|

620 – 700

|

Needs improvement and steady usage to rectify.

|

Average

|

|

700 – 750

|

A workable score can be applied for credit.

|

Good

|

|

750 – 800

|

A good credit score is the benchmark required by Banks.

|

Very Good

|

|

800 – 900

|

Optimum score with an impressive credit history.

|

Excellent

|

|

|

|

| Score Band |

Significance |

| CIBIL Score of 0 |

Denotes NIL Credit Usage. |

| CIBIL Score of -1 |

Insufficient length of Credit usage below 6 months |

| Below 300 |

Below six months of credit usage |

| 300-550 |

Low score not eligible for credit |

| 550-620 |

Credit issues. Poor credit history |

| 620-700 |

Needs improvement and steady usage to rectify. |

| 700-750 |

A workable score can be applied for credit. |

| 750- 800 |

A good credit score is the benchmark required by Banks. |

| 800-900 |

Optimum score with an impressive credit history. |

CIBIL Score Requirements for Personal Loan

- A stable credit and a CIBIL score range of 750+ are required to apply for an unsecured, collateral-free personal loan.

- Applicants with a 0 or -1 CIBIL score can apply for a personal loan to HDFC Bank/ ICICI Bank if they meet the eligibility criteria.

- The CIBIL score requirement differs from lender to lender and depends on the terms.

- Banks accept a lower CIBIL score if the applicant has a credit relationship or applies based on a fixed deposit held.

What is a CIBIL Score for Secured and Unsecured Credit?

- Banks consider the CIBIL score and history when processing all credit lines, secured and unsecured loans.

- A personal loan and a credit card are unsecured and provided based on a customer’s profile; therefore, emphasis is placed on a high CIBIL score and the customer’s credit history.

- A secured loan, such as a home loan, a loan against property, or a vehicle loan, is secured by a mortgage. It may be easier for a customer to get a secured loan with a lower or nil CIBIL score.

- Banks may consider a mortgage request for an applicant with a below-average CIBIL score of 650 points and above, but applicants with a delinquent record or settled loans will have to apply to an NBFC.

Read More : NBFC Vs Bank Personal Loan

Have the CIBIL Score Requirements Changed?

- The CIBIL Score has become a priority for Banks and NBFCs, as keeping delinquencies and defaults below the acceptable percentage is essential.

- With the introduction of online credit platforms, application loans, and the granting of licenses to new NBFCs, the options for customers to get instant credit have increased the risk of customer defaults.

- The acceptable CIBIL benchmark has increased from 720 points to a minimum of 750 points, which is required to get an ICICI Bank credit card or an HDFC Bank personal loan.

- Banks check the customer’s credit obligations and CIBIL history for personal loan eligibility. If the customer’s existing dues exceed the FOIR, the request for additional credit is declined.

Can you get a Loan without a CIBIL rating?

- Personal loan applicants and credit card seekers can apply without a CIBIL score to a Bank that accepts a 0 or -1 CIBIL score, provided they fulfil the other eligibility criteria.

- Customers who are new employees or who have a salary account with the Bank are issued a personal loan without a credit rating. Though the credit limit or loan amount issued will be limited.

- Applicants over 30 years old without a CIBIL score are viewed negatively, and lenders assume they have changed credentials to cover a default.

- Secure loans such as Home Loan, Loan Against Property, or Vehicle Loan are granted without a CIBIL score if the applicant has stable employment and residence.

Can You Get a Loan with a Lower Score?

- It may be possible to get a loan against security rather than an unsecured loan if you have a lower CIBIL score.

- Apply to an NBFC willing to issue the loan amount you require, but charge a higher interest rate.

- Work on improving your CIBIL score by repaying debts on time and rebuilding your score

Practices that Impact a Credit Score

1. Honour the payment due date for the credit taken.

- Be vigilant about the due date for your Credit Card dues or the EMI for your loan.

- Ensure there are sufficient funds in your salary account to clear the EMI on the scheduled date.

- If there is a lapse, make the payment as soon as possible.

2. Do not apply for credit indiscriminately.

- 10% of the CIBIL score is allotted to the number of enquiries received from lenders.

- Check eligibility criteria and interest rate before applying for a loan or credit card.

- Each credit enquiry by a lender will negatively impact your score by 10 to 15 points.

3. Maintain a Healthy Mix of Secure & Unsecured Credit

- A secure loan, a loan against property, or a Home Loan with a vintage adds stability to your Credit Score.

- Unsecured credit, such as a personal loan or a credit card, can help boost a credit score quickly.

- All credit accounts that have been repaid on time and closed successfully add to the CIBIL score.

What is a CIBIL Score for Personal Loan Eligibility?

- The CIBIL score check has become a mandatory eligibility criterion for the personal loan process.

- A self-check at www.CIBIL.com before applying for a personal loan will help confirm eligibility, without negating the score.

- A CIBIL score of 750 or higher will ensure approval from most Banks.

- If your CIBIL score does not meet the benchmark, check for a suitable lender before applying.

Read More: Personal Loan Eligibility

In conclusion, with our policy of ‘Customer First,’ we at www.yourloanadvisors.com prioritise understanding our customers’ profiles, credit histories, and needs. If the CIBIL score is not up to the mark, we offer them relevant options and help them to apply to the most suitable Lender. Over the years, we have helped and guided customers to fulfil the Personal loan eligibility criteria before applying, so they are granted the funds they need. Get in touch with us if you need help deciphering your CIBIL score and improving it!

91-9711165183

91-9711165183

May 12, 2026

May 12, 2026