91-9711165183

91-9711165183

July 25, 2023

July 25, 2023

The growing figures prove that credit usage is increasing dependency on loans and credit cards for lifestyle needs and growth is now the norm.

Did you know that the value of loans in India rose by 16.20 % year-on-year in the fortnight ending 30th June 2023?

Individuals with a Personal or Home Loan can borrow additional funds as a Top Up. A Top Up is quick and convenient, but Applicants should not take approval for granted and must consider the policy criteria of the Lender.

Banks do their due diligence when awarding an extra amount as Top Up Loan Requirements. The process may vary slightly depending on the specific Lender and their policies, but generally, here are the policy and the steps for the processing of a Personal Loan Top-up.

Appropriate Gap: Banks offer a Top Up Loan within 3 to 6 months after issuing the primary loan. This interval allows the Bank to evaluate the customer’s behaviour.

Financial Eligibility: The customer’s earnings should support the mandatory expenses and obligations, such as Credit card bills and loan instalments. With surplus funds to afford an additional EMI for the Top Up. Customers can check the same with the Top Up Loan EMI Calculator.

Existing Personal Loan Track: The payments of the existing Personal Loan must be on time. Lenders are more than willing to give an additional loan to applicants repaying their EMI on the due date.

Credit Score and History: The applicant’s CIBIL Score must be above 720 points. The Bank will view the CIBIL of the applicant to ensure there are no recent defaults or excess credit appended recently.

Employment Status: The current employer should feature in the company category list of the Bank. The Bank evaluates the Top Personal Loan Top-up.

Up request according to the present job profile of the customer. Having a consistent employment history can be beneficial in obtaining a Personal Loan.

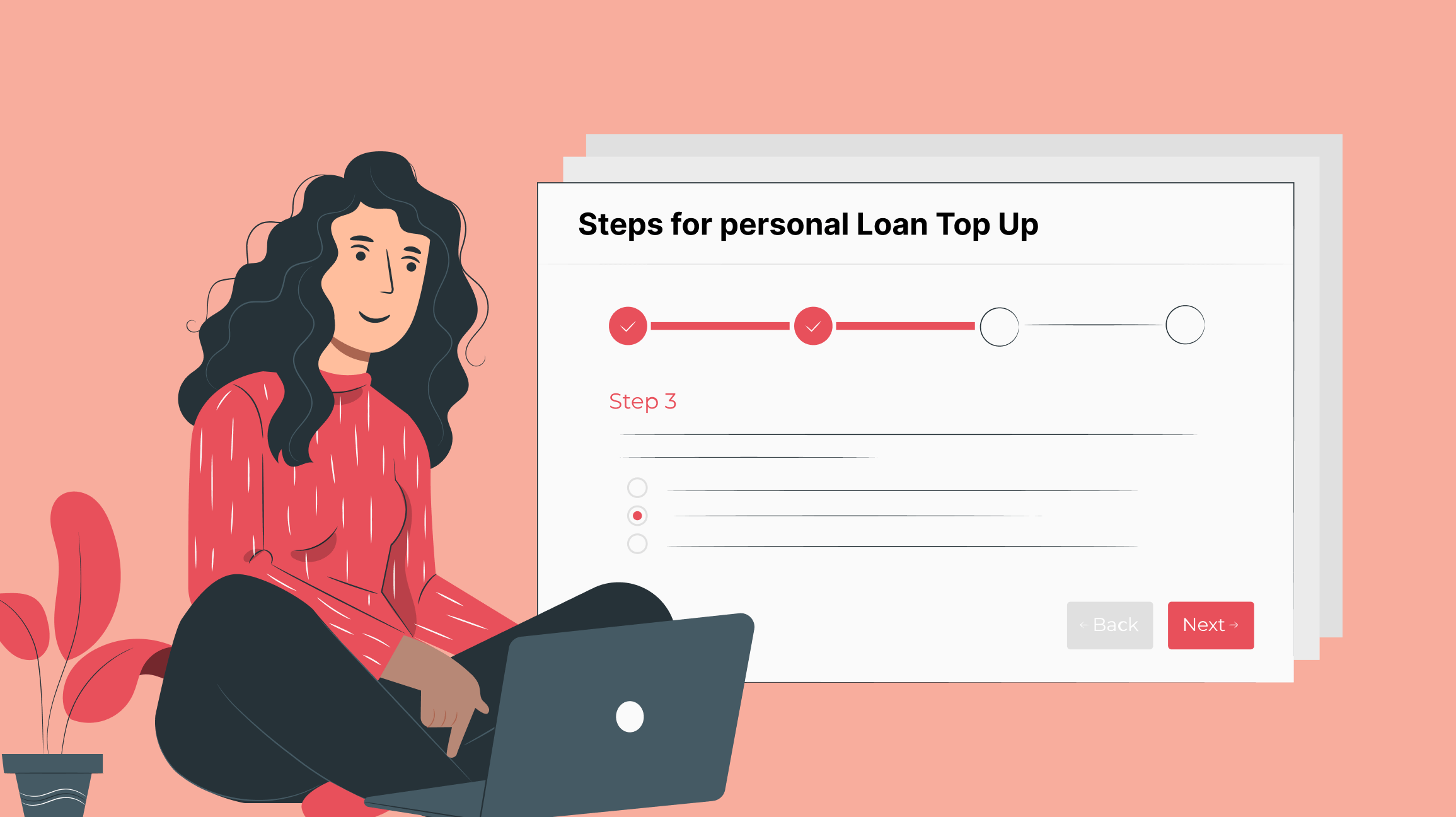

Need funds and ready to Apply for a Top Up Personal Loan? The process stages are listed below:

Before Applying for a Top Up to the Bank, determines your requirement and the financial bandwidth to pay the instalment. Remember, the total loan amount (original loan + top-up) cannot exceed the maximum loan amount allowed by the Lender.

Documentation: The Bank requires fresh documents to Process a Top Up Loan. The documentation is similar to a new loan, such as the proof of income, identification documents, bank statements, and any other documents the Lender specifies. The request for a Top-up is considered based on the latest records.

Application: To apply, a customer may complete the necessary information in the form online or manually and submit the same with copies of the documents required. The data filled in the application must match the documentation.

The Lender will acknowledge the request and issue a control number the processing of a Top Up Loan is similar to a new loan and includes the following steps:

The Top Up to the existing loan begins after the request for an additional loan amount is approved.

The Lender constructs a new Personal Loan with the principal balance of the existing loan and the Top Up amount approved and presents a fresh instalment. The new instalment will replace the previous EMI for the appointed tenure.

The Bank follows a formal process and only accepts a request if the application fulfils the eligibility for a Top Up Loan. Therefore, comparing the terms offered by other lenders before taking a Top Up is advisable.

A Top Up Personal Loan has its advantages if the customer has a successful Personal Loan existing with the Bank additional amounts are granted timely. Banks would like to retain good Customers by offering better terms for the loan.

All is not hunky dowry. A Top Up has its drawbacks. The nature of the existing loan changes and a new repayment schedule for the fresh loan is instated. The Bank disregards the interest paid previously for the principal balance. Work out the complete costs for the loan.

The foreclosure and part payments are allowed after 12 instalments; Banks renew this period with the new loan. Customers wanting to repay their loans should look at other options.

The applicant has a choice and must consider other options, such as a Parallel Loan from the same Bank or a new loan with another lender.

Apply For Top up Personal Loan

How To Check Your Eligibility For a Top up Loan

When Can a Personal Loan Top Up Cost More and What are The Options