91-9711165183

91-9711165183

January 15, 2026

January 15, 2026

A credit score or CIBIL history check has become a vital part of the lending process. Lenders will request your credit report from CIBIL before proceeding with your Personal loan application. If your score does not meet the necessary benchmark, your request can be declined.

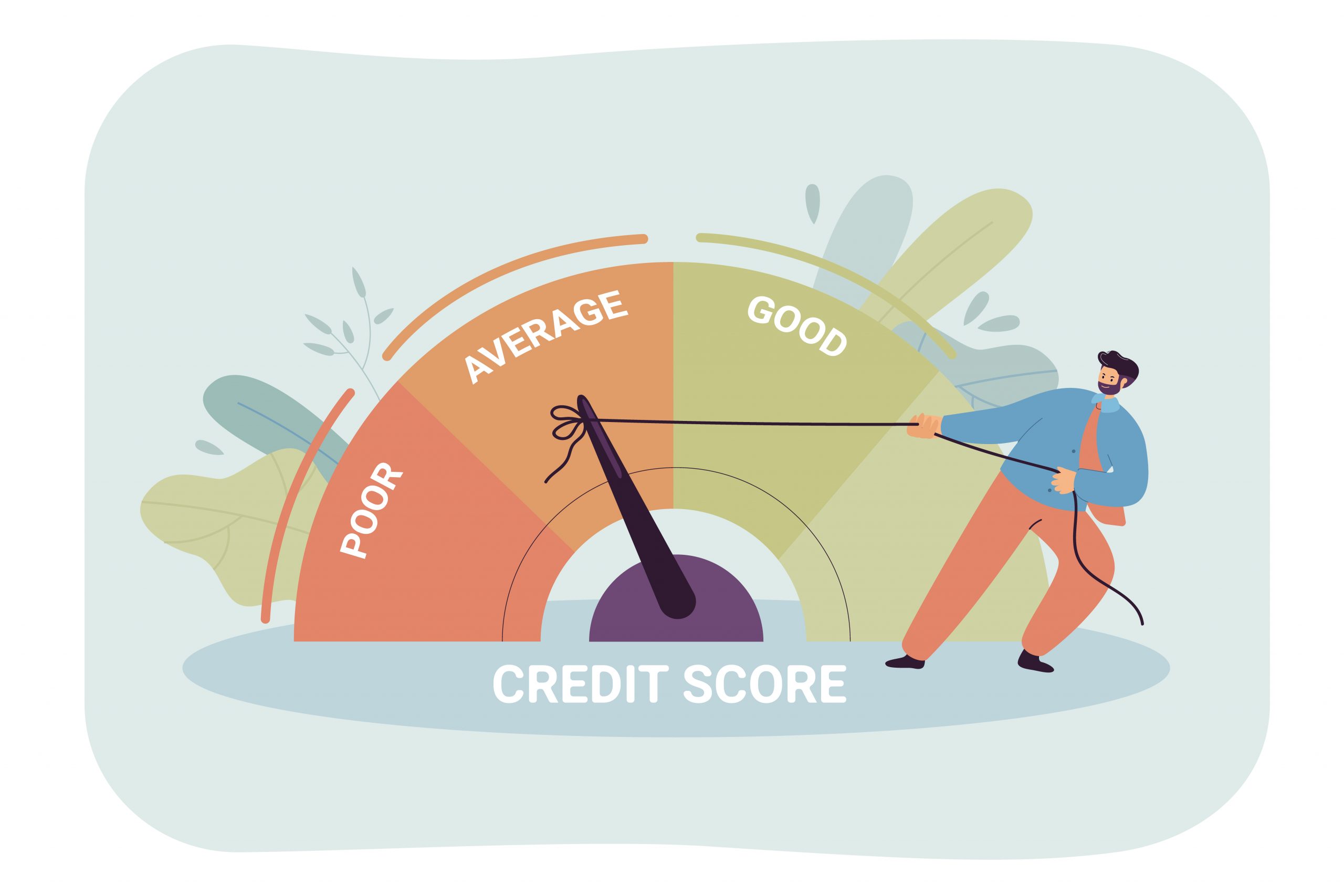

A numeric score is issued by CIBIL, ranging from 300 to 900 points, based on an individual’s credit usage. A credit score of 720 points and above is considered a healthy score by banks for issuing credit. Depending on the repayment history and credit usage, you are issued a score by major bureaus recording credit transactions, which can be interpreted as follows;

600 to 650 points: if your credit score hovers between the 600 and 650 mark, this means:

A score of 600 to 650 points is considered below average by lenders, and obtaining further credit may be difficult.

650-700 points. Any score above 650 points is a fair score, though the lender will look into the details of the credit history for the reason for the dip in score, which could be any of the following:

700-750 points: Although a 720 CIBIL score is the required benchmark by Banks, any score above 700 points will make you eligible for a personal loan.

750 points and above: A CIBIL score of 750 points and above is the mark of successful credit management.

If you need additional funds as a personal loan and are currently facing rejections due to a low credit score, you can avail of the following options:

Apply to a Bank with an account or a credit relationship: If you have an account with a Bank and maintain a good balance, or have previously repaid credit successfully, apply for a personal loan online; the chances are that the credit team might approve a personal loan.

Apply for a smaller amount or choose an NBFC that charges higher interest rates: If you know your credit score is lower than needed, there is no point in applying to other lenders, as this can further damage your credit score. Seek an NBFC that provides unsecured loans with lower credit score requirements, even if the interest rate is higher, as this will help you overcome your cash flow issues.

Apply with a co-applicant: A guarantor or a co-applicant with a good credit rating and income can strengthen your Personal loan application. As a personal loan is unsecured funding, having a co-applicant with a healthy financial track record can reassure the lender that the repayment will be made on time.

Apply for a Personal loan against securities or fixed deposits: If you hold funds in fixed deposits with a Bank, it will strengthen your personal loan request. Banks offer up to 80% as a loan against the amount held as a deposit or security. Banks are reassured that they have funds in safekeeping to recover the loan if required. Therefore, the clause of a downgraded CIBIL score will be overlooked.

Check your credit score regularly: Do not let it come as a surprise; a free credit score check is readily available at www.CIBIL.com. It is helpful to check your credit score before applying for further credit to understand your current standing. In case there is an error, you can take steps to rectify it.

Circumstances may have led to a fall in your credit score, but all is not lost. Take the following steps to get your credit score back on track.

Repay pending dues: Clear outstanding accounts by paying outstanding amounts and closing them.

Transfer credit card dues: Apply for a balance transfer of credit card dues via an AXIS Bank personal loan to avoid paying an inflated interest rate. The loan amount can be repaid easily with a reasonable EMI.

Timely EMI payments: Ensure there are sufficient funds in your account to clear the EMI for existing loans.

Rebuild your CIBIL score: Take steps to rebuild your credit score by applying for a secured loan and making timely repayments.

Usage of unsecured credit: Work on increasing your score by using your credit card judiciously and paying off the balance on the due date. Regular usage of a credit card with timely payments can help to increase your score quickly.

Keep your debt-to-income ratio intact: Avoid excessive credit use, live within your means, and create a budget to ensure you have the funds on hand to repay the credit you use.

Getting over a bad credit phase and improving your credit score are not easy. To give individuals an opportunity to improve their current credit rating, the RBI (Reserve Bank of India) has instructed credit rating agencies to remove details of accounts that are more than 7 years old.