Personal Loan

Professional

Merchant Navy

ICICI Bank

Locations

Delhi and NCR

Gurgaon

Ghaziabad

Faridabad

Noida

Greater Noida

HDFC Bank

Golden Edge

Parallel loan

Company list

Locations

Delhi and NCR

Gurgaon

Ghaziabad

Faridabad

Noida

Greater Noida

AXIS Bank

Locations

Delhi and NCR

Gurgaon

Ghaziabad

Faridabad

Noida

Greater Noida

YES Bank

Locations

Delhi and NCR

Gurgaon

Ghaziabad

Faridabad

Noida

Greater Noida

Balance Transfer

HDFC Bank

ICICI Bank

KOTAK Bank

AXIS Bank

Top Up

ICICI Top Up Loan

HDFC Top Up Loan

Axis Top Up Loan

Yes Top Up Loan

EMI Calculator

Rate Of Interest

Personal Loan Eligibility Check

Eligibility Calculator

Business Loan

Loan Against Property

Blogs

Credit Cards

Company list

91-9711165183

Blogs

Do stay in touch for the latest in Product details, updates, and news!

April 28, 2026

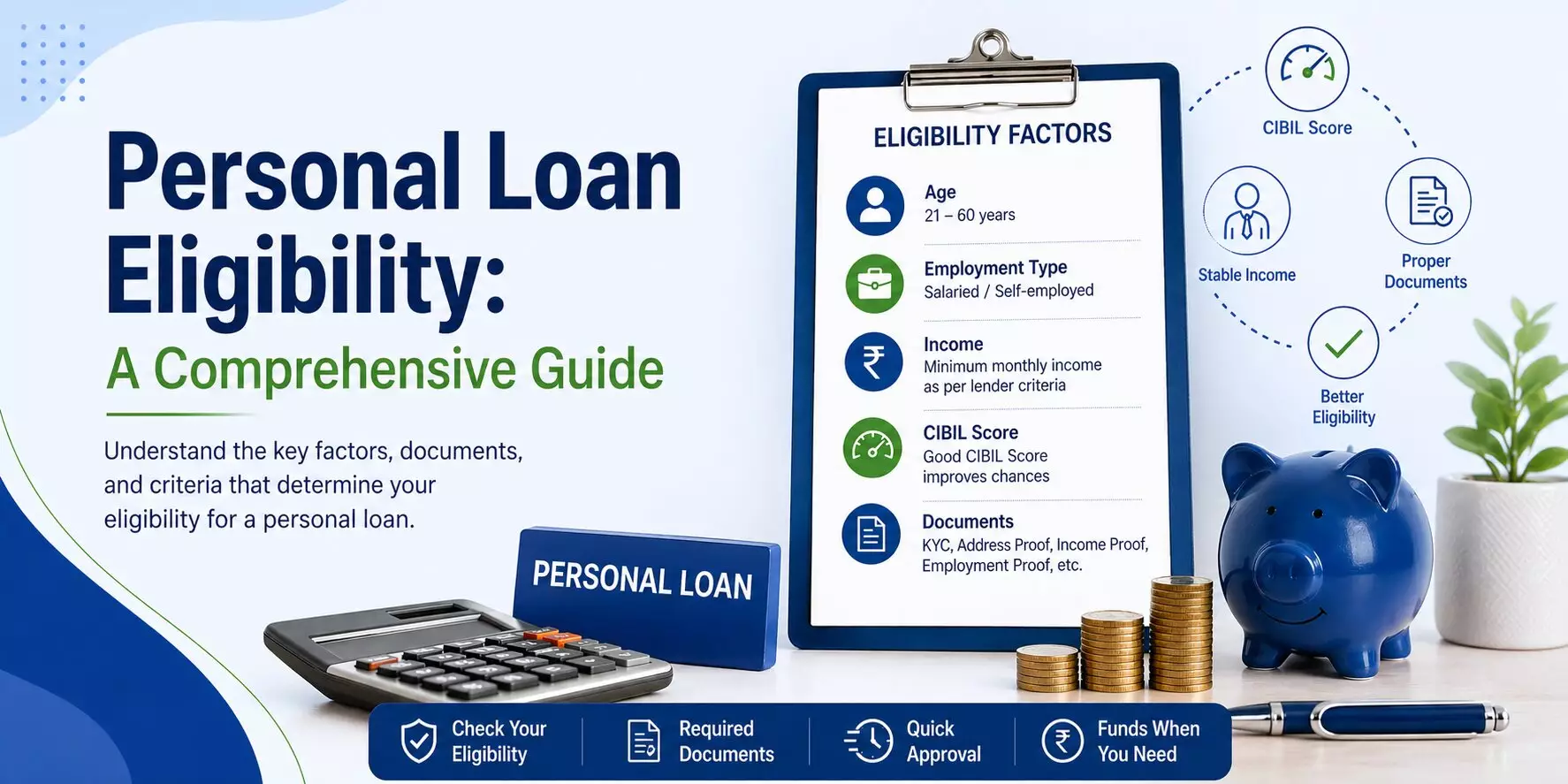

Personal Loan Eligibility: A Comprehensive Guide

By admin

Read More

March 10, 2026

What Are the Key Disbursal Documents for a Personal Loan?

By admin

Read More

February 21, 2026

What are the 3 Top CIBIL Reasons for a Personal Loan...

By admin

Read More

February 12, 2026

Top CIBIL-related queries for a Personal Loan

By admin

Read More

January 30, 2026

NBFC Vs Bank Personal Loan

By admin

Read More

January 22, 2026

Understanding HDFC Bank Personal Loan Top-Up

By admin

Read More

January 15, 2026

How can I get a personal loan if I have a...

By admin

Read More

January 8, 2026

Company category list versus Credit score

By admin

Read More

1

2

3

…

20

>

Connect with us

What is 3 + 2 ?

Answer for 3 + 2

Δ

Search

Categories

Business Loan

CIBIL Diary

company category list

Credit Card

EMI

HDFC Bank

Home Loans

ICICI Bank

Merchant navy

News Updates

Personal Loan Balance Transfer

Personal Loans

Top Up Personal Loan

Uncategorized

Popular

Posts

HOW TO USE A LOAN EMI CALCULATOR?

Why Your CIBIL Score Matters More Than You Think

Reasons For Rejection of a Personal Loan

Connect with us

What is 1 x 4 ?

Answer for 1 x 4

Δ