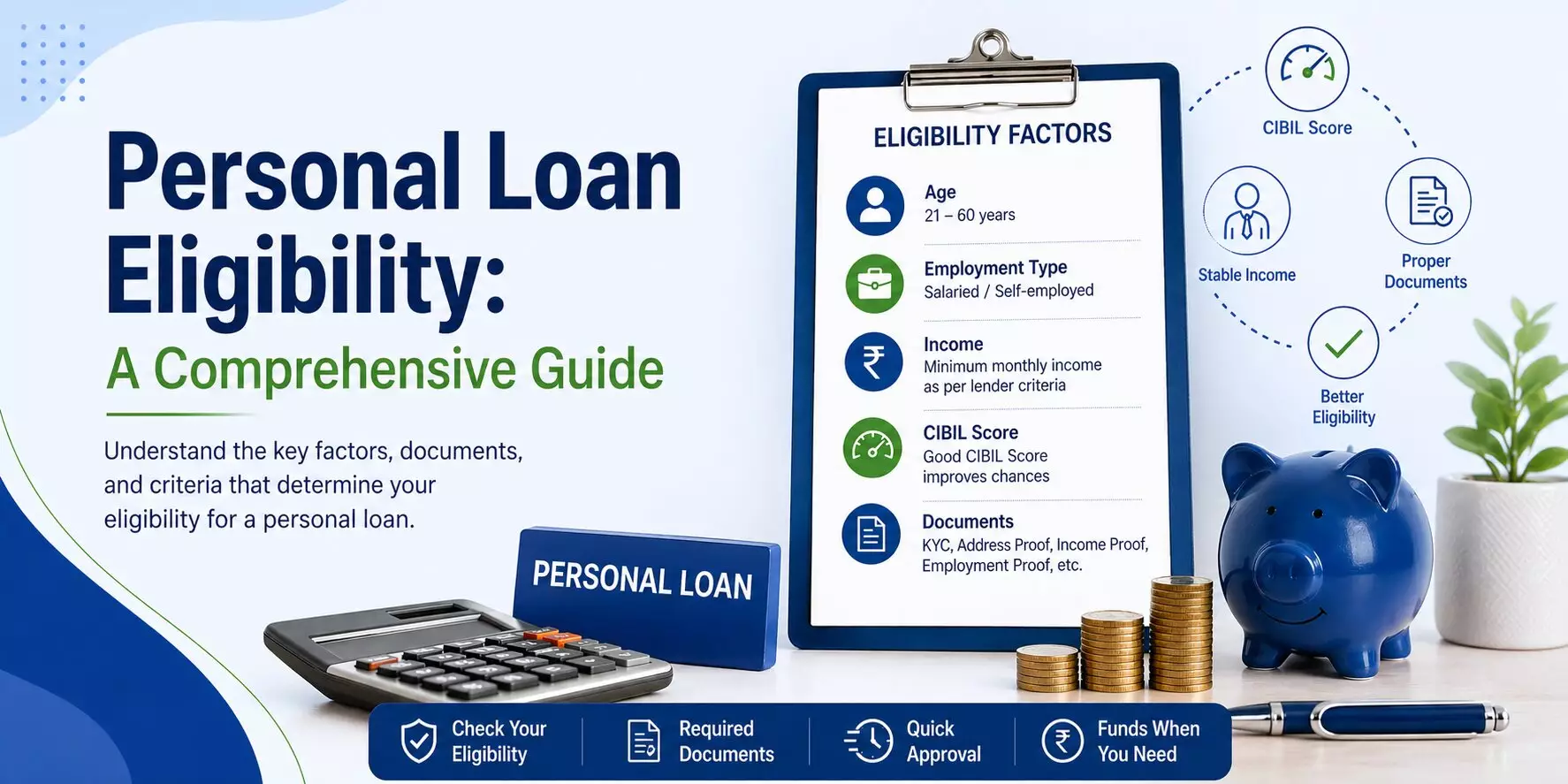

Applying for a personal loan is now quick and simple, but it cannot be assumed that you will be approved for the loan amount you need. Enumerated below are the key features and know-how on Personal Loan eligibility that have been explained for your assistance.

A personal loan for salaried individuals has become the most popular choice for funding lifestyle expenses and emergencies. The ease of online applications and quick processing has made personal loans more accessible. A personal loan is issued based on the applicant’s eligibility. The primary considerations for personal loan eligibility are

- Applicant’s Income

- Monthly salary credited to the bank account

- CIBIL score

- Existing liabilities (debt, credit card dues, etc)

- Employer’s category as per the HDFC Bank-approved company list for personal loans.

Banks and NBFCs provide personal loans ranging from 1 lakh to ₹₹ lakhs. Loan amounts are determined by the applicant’s profile and the lender’s policies. Given below is an illustration of the minimum and Maximum Loan amounts offered by Banks and NBFCs.

Personal Loan Eligibility Calculator

You are not eligible due to age criteria (21-60 years).

What is the income required for personal loan eligibility?

The minimum income threshold required by banks and NBFCs varies by lender and applicant location. The income determines the loan amount the applicant qualifies for, the interest rate applied, and the relevant FOIR.

- Applicants with a Salary of ₹ 20k+ are eligible from Tier 2 and Tier 3 cities, as well as INCRED Finance.

- Applicants with a Salary of ₹ 25k + can apply to YES Bank, select NBFCs, SMFG Finance, and Poonawala Finance.

- Applicants with a salary of ₹ 30k+ are eligible to apply for a personal loan with HDFC Bank and AXIS Bank.

- ICICI Bank requires a minimum salary transfer of ₹ 40k+ to process a personal loan.

| SALARY |

BANK/NBFC |

LOAN AMOUNT |

INTEREST RATE |

| > ₹ 20,000 |

INCRED |

Up to ₹ 3 Lakhs |

25% -30% |

| ₹ 25000 + |

YES Bank, SMFG Finance, NBFCs |

Up to ₹ 4 Lakhs |

15%- 25% |

| ₹ 30,000 + |

HDFC Bank, AXIS Bank, KOTAK Bank |

Up to ₹ 7 Lakhs |

12% – 14% |

| ₹ 40,000 + |

All Major Banks |

Up to ₹ 10 Lakhs |

10% – 12% |

What are the exceptions made by financiers for salary credits?

- AXIS Bank accepts salary credits of ₹20k or more for an AXIS Bank salary account holder.

- Applicants employed with companies that do not appear on ICICI Bank’s approved company list should have a regular salary credit of ₹ 1 lakh or more.

Suggested Read : Personal Loan Eligibility Based on Salary

How much EMI am I eligible to pay?

Banks consider your income and expenses to determine your EMI, helping you feel more in control of your loan options. Applicants can calculate their EMI using the EMI Calculator before applying for a personal loan to get an idea of the amount they can comfortably pay towards the monthly instalment. Banks and NBFCs most widely use the FOIR method to confirm an applicant’s eligibility to pay EMI.

The role of the FOIR (Fixed obligations versus Income)

The FOIR determines the maximum monthly EMI the applicant can afford. The fixed obligations include fixed monthly costs, existing loan EMIS, and credit card dues, all of which are deducted from the income.

The formula used to calculate the FOIR.

Total Monthly Obligations/ Net monthly income * 100 = FOIR.

Example:

- EMI for Loan and Credit card obligations = ₹ 30,000/-

- Net Salary = ₹ 60,000/-

- FOIR = 0.5% * 100 = 50%

The above is the general rule for further processing the FOIR application; salaries have been segmented as follows.

| SALARY |

FOIR |

Maximum EMI Allowed |

Tenure |

| ₹ 20,000 to ₹ 40,000 |

40% to 50% |

₹ 8000/- to ₹ 10.000/- |

12 months to 60 months |

| ₹ 40,000 to ₹ 75,000 |

50% to 60% |

₹ 20,000/- to ₹ 40,000/- |

12 months to 60 months |

| ₹ 75000+ |

70% |

₹ 45000/-+ |

12 months to 72 months |

Key features of the FOIR include

- High-income applicants have higher disposable income after accounting for monthly expenses and are thus allotted a FOIR of 70% to 75% of their monthly income.

- Companies included in the upper tier of HDFC Bank’s company category list, such as Elite Super A and Cat A companies, are given additional leverage.

- Companies listed as Category C and D are allotted lower multipliers and are eligible for lower personal loan amounts, which are capped.

Suggested Read: How to reduce current EMI ?

How does employment influence the Personal Loan eligibility?

The stability and reputation of your employer significantly influence your Loan eligibility, as banks prefer to lend to employees of established, profitable companies with consistent employment records.

Profile of Employer

Lenders look to fund employees of established companies with increased profitability, infrastructure, and employment. Employees of companies that are Limited, Private Limited, PSUs, and Government organisations are eligible for personal loans from most banks and NBFCs. In contrast, employees of proprietorship and partnership firms are not.

Company Category

Applicants whose employer is listed in the Approved Company Category list of Banks are eligible to apply for a personal loan, such as:

- HDFC Bank Company Category List.

- ICICI Bank List of Approved Companies.

- AXIS Bank Approved Company List.

Companies that feature in the upper tier of the list, such as CAT A or Super A companies in the HDFC Bank Company Category List, are allotted higher multipliers for calculating eligibility for Personal Loan amounts than CAT C or CAT D companies.

AXIS Bank and ICICI Bank also apply a higher FOIR of up to 70% for the Loan amount eligibility for Personal Loans.

Vintage of Employment

A work experience of 12 months or more is required to be eligible to apply for a Personal Loan. New appointees are issued restricted loan amounts, while Employees with vintage work experience are considered stable and secure and can be awarded a Personal Loan of ₹10 lakhs or more.

Salary proof

With the onset of Digital banking systems, banks now require a direct salary transfer to the salary account regularly for a period of 3 months or more to apply for a personal loan. Proof in the form of a Bank statement reflecting salary credits is required when applying.

Key Features of the Tenure affecting the Personal Loan eligibility

The repayment term for a Personal loan or Tenure ranges from 12 to 72 months.

Longer Tenure

A longer tenure can give you a sense of control, increase your eligibility, and make monthly payments more manageable. Applicants employed with the listed companies are issued an extended tenure of up to 84 months.

Shorter tenure

Applicants who wish to repay their Personal Loan sooner can opt for a shorter tenure, thereby saving on interest. The condition is that the EMI does not exceed the Bank’s debt-to-income ratio limit.

Illustration of the EMI calculation based on the tenure

- The EMI payable by the applicant depends on the repayment tenure. If the applicant requests a shorter tenure, the eligible loan amount decreases. If the EMI exceeds the FOIR, the tenure can be extended or the loan amount reduced, for example:

(Hypothetical customer details)

- Customer name: Archana Singh.

- Age: 35 years

- Employer: TELEPERFORMANCE GLOBAL SERVICES PRIVATE LIMITED (Listed as CAT B in the HDFC Bank Company Category List)

- Marital Status: Married

- Salary Account: HDFC Bank.

| Net Salary |

₹ 60,000/- |

| FOIR Applicable 55% |

₹ 35000/- |

| Current Obligations |

|

| Existing Home Loan EMI |

₹ 20,000/- |

| Credit card outstanding |

₹ 50,000/- |

| 5% of outstanding credit card balances are treated as obligations. |

|

| Current Obligations total |

₹ 22500/- |

| Eligible to pay an EMI of |

₹ 12500/- |

Eligibility Calculation with varied tenure

(Interest Rate applicable at a monthly reducing balance)

| Tenure |

Interest Rate |

EMI |

Maximum Loan amount |

| 60 months |

10.50% |

₹ 12,896.34 |

₹ 6,00,000 |

| 48 months |

10.50% |

₹ 12,801.69 |

₹ 5,00,000 |

Existing Liabilities

- The customer’s existing obligations or liabilities are noted by retrieving the CIBIL report and reviewing the Bank Statement. The personal loan amount approved is finalised after deducting the obligations.

- The EMI paid for the existing loans. If the customer is a co-applicant on a loan, banks will consider 50% of the EMI as the customer’s obligation. Certain NBFCs may not include the obligations as a co-applicant for calculating the Personal Loan eligibility.

- If the App’s (Application loans) obligations exceed the Lender’s limits, the Lender will declare the customer overleveraged and decline the personal loan request.

- All credit dues, whether as a primary or an add-on cardholder, form part of the obligations. 5% of the credit card dues are included in the liabilities. If the pending card dues reflected in CIBIL are over 5 times the monthly salary, the personal loan request is declined.

- Salaried applicants nearing retirement age (62) are offered a limited tenure, which restricts their eligibility for a higher loan amount. Younger applicants working in listed companies are allotted longer tenures and higher Personal Loan amounts.

- If the applicant resides in a self-owned or family home, the applicant’s personal loan eligibility will increase in the absence of a rent liability.

CIBIL

- The trust factor for an unsecured Personal Loan increases with a CIBIL score of 750 or above. This can boost your confidence, as banks feel more assured in offering higher loan amounts for maximum tenures.

- Customers who are first-time loan seekers without a CIBIL score are allotted an apprehensive loan amount. A CIBIL score is required for Customers aged 35 or older to be eligible for a personal loan.

- If your CIBIL score is below 650 points, it is advisable to improve your CIBIL score before applying for a Personal loan to avoid rejections and further damage to your CIBIL score.

How to improve your Eligibility for a Personal Loan

Consider the following factors to increase your eligibility;

- Maintain a CIBIL score of 750+ and repay all your Credit Card dues.

- Pay back and close any pending loans and those nearing the end of their tenure.

- Include all sources of income and the income of an earning spouse or parent.

- Apply to the Bank with a salary account or a successful credit repayment record.

- Do not make multiple inquiries at once, as you may be branded as credit-hungry.

- Consolidate multiple loans via a balance transfer to improve FOIR.

Check out a Live example of increasing eligibility with the assistance of www.yourloanadvisors.com

Nitin Khanna (Name Changed for privacy) contacted us via our website for assistance, as he urgently needed funds of ₹ 400000/- lakhs for his wedding celebrations. He is employed with a company listed as CAT B in the HDFC Bank company Category list, with a salary of ₹ 3500/- transferred to ICICI Bank.

His personal loan request to ICICI Bank was declined due to overleveraging. Given below are his financial details:

| Income |

₹ 35000/- |

| FOIR applicable 50% |

17500/- |

| Home Loan EMI |

13000/- |

| Eligible to pay EMI of |

4500/- |

- He was considered overleveraged due to his home-loan EMI obligations.

- We further enquired about the status of his co-applicant on the home loan.

- He revealed his father was a co-applicant who was earning a salary of ₹ 50,000/-

- As his father was an earning co-applicant, we asked the Bank to reconsider his request and submitted his father’s documentation as proof.

- As per policy, banks treat 50% of the home loan EMI as an obligation if the applicant has a regular income.

His eligibility calculations with 50% of the home loan EMI obligated were now as follows;

| Income |

₹ 35000/- |

| FOIR applicable 50% |

17500/- |

| Home Loan EMI |

6500/- |

| Eligible to pay EMI of |

11000/- |

Thus, his request was reconsidered and sanctioned for:

| Loan Amount Required |

₹ 400000/- |

| EMI for 48 months |

10338.21 |

Usage of the EMI Calculator for Personal Loan Eligibility

The EMI calculator is a useful tool that helps you calculate the EMI for the loan amount you require. Key inputs include:

- The Principal Loan amount required.

- The interest rate.

- The tenure.

Thus, you can confirm the EMI to be paid for the personal loan amount required before applying for a Personal Loan. This will help you check whether the EMI is affordable, and if the EMI is too steep to pay along with the other existing credit and expenses, you have an option to:

- To ask for an extended tenure.

- Apply for a lower Personal Loan amount.

- Check with other lenders for a lower interest rate.

- Consolidate your existing debt.

April 28, 2026

April 28, 2026